In portfolio construction, investors typically focus on equities for growth and don’t account for crisis protection. But over two decades of Indian market behaviour reveal something important.

Debt – an often overlooked asset class, quietly improves portfolio resilience.

Across market drawdowns, asymmetric crashes, and trend reversals, liquid debt has consistently delivered what no other asset class can match – capital stability, immediate liquidity, and a steady positive return irrespective of market conditions.

A closer look at the data from 2005-2025 shows why liquid debt is indispensable for robust, rule-based investment frameworks.

1. The stability premium: What 20 years of data tells us?

From 2005 to 2025:

Average Annual Returns

Debt: ~7.23%

CNX500: ~20.45%

Equities clearly dominate on long-term return – as they should.

But these numbers miss the deeper structural insight:

Liquid debt’s returns have an extremely tight distribution (5-9% range), while equity returns swing between +88% and -57%.

This volatility gap is the foundation of its value.

Liquid debt doesn’t try to beat equities – it protects investors from the cost of being wrong at the wrong time.

2. When debt outpeforms: The only years that matter

Outperformance isn’t measured by how often an asset beats equities in a bull market – equity always wins those.

What matters is who protects the portfolio during crashes.

Analysing 20 years of data showed the following picture:

Years in which debt outperformed CNX500:

2008: +8.38% vs -57.13%

2011: +9.13% vs -27.19%

2015: +7.38% vs -0.72%

2018: +6.75% vs -3.38%

Debt outperformed equities in 4 out of 21 years (~19%), and every single instance was during an equity stress regime.

This pattern is structurally important. Whenever CNX500 breaks trend, liquid debt becomes the top-performing asset class.

This aligns perfectly with our monthly analysis, where the returns for CNX500 and Debt were studied for over 240 months, and we found that debt beat equities in 106 months out of the 241 months studied. (~44%).

All its wins cluster during market weakness. This is exactly the behavior risk-conscious portfolios depend on.

3. Low correlation: The mathematical edge

We studied the monthly returns of CNX500, Gold, Silver, and Debt from October 2005 to October 2025. The correlation shows:

Asset Correlation with CNX500

Gold – 0.086

Silver 0.166

Debt – 0.086

Liquid debt has the same negative correlation with equities as gold, but without the volatility gold introduces during rate cycles.

This means:

- It does not move with markets

- It does not deepen drawdowns

- It smoothens the return curve

- It enhances resilience during sharp reversals

Correlation is foundational in momentum portfolios – and liquid debt is one of the most reliable diversifiers available.

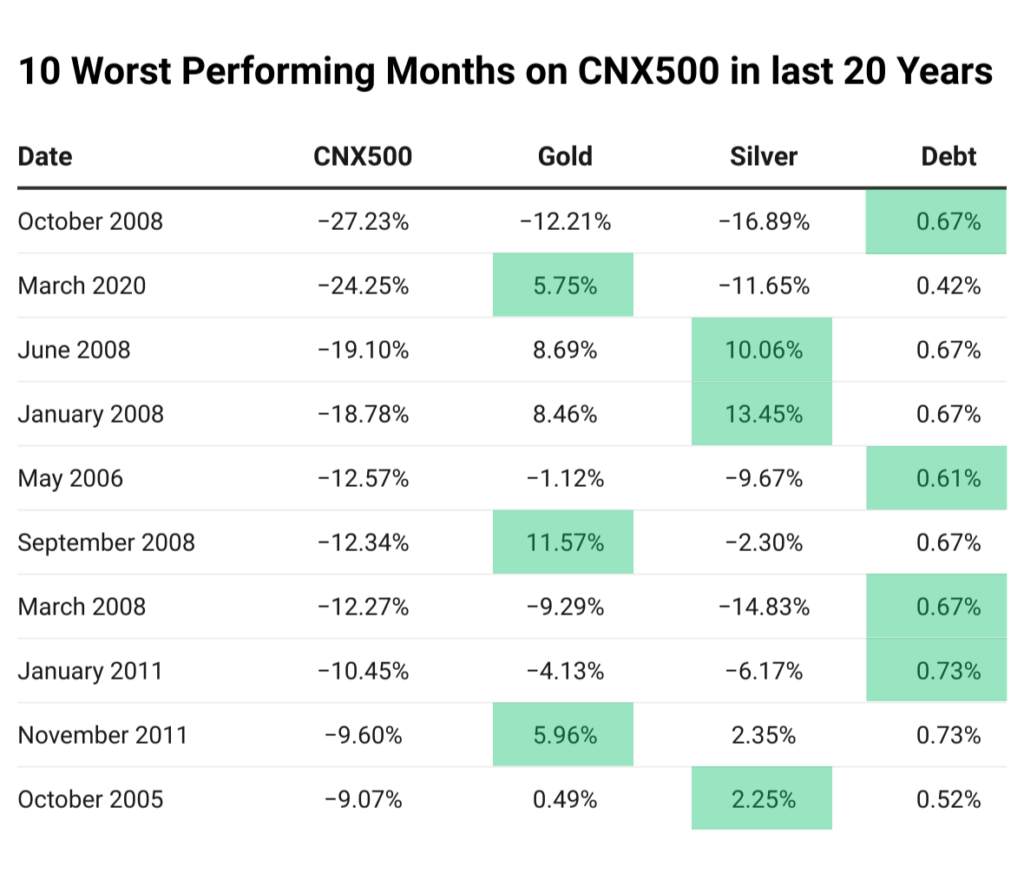

4. Stress-test performance

We extracted a dataset of severe market falls, which showed CNX500 plunging between -9% and -27% in multiple months across years like 2008 and 2020.

During these exact same months:

- Gold was mixed

- Silver was unpredictable

- Debt delivered +0.4% to +0.7% reliably

- While equities were collapsing double-digits, liquid debt quietly compounded.

This alone justifies its presence. But the real insight emerges when we see it in a multi-asset portfolio.

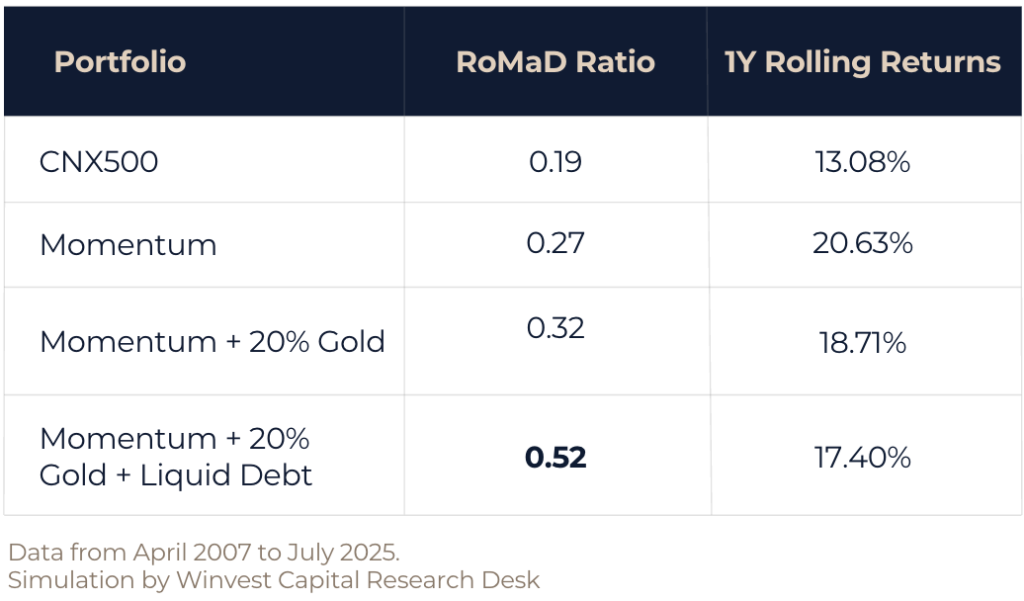

5. Portfolio A/B/C: How liquid debt transforms risk?

Using data from 2007-2025, we compared 3 model portfolios:

A: Momentum

B: Momentum + 20% Gold

C: Momentum + 20% Gold + Liquid Debt

Where,

Momentum – NIFTY200 Momentum 30 | Gold – Nippon Indian GoldBees | Liquid Debt – Nippon India LiquidBees.

Adding gold helped.

Adding liquid debt changed the entire portfolio behaviour.

Portfolio C delivered:

- The lowest drawdowns,

- The smoothest recovery curve,

- The highest resilience-to-return ratio, and the best stability for a momentum-driven strategy.

This is the essence of modern portfolio construction.

6. Why liquid debt works: more than just safety?

Liquid debt provides four advantages no other asset class can combine:

- Dry Powder: Immediate deployability during dislocations.

- Forced-Selling Protection: Preserves portfolio integrity when equities fall sharply.

- Tactical Buffer: Enables discipline in systematic strategies; avoids whipsaw-driven drawdowns.

- Volatility Reduction: Sharply improves risk-adjusted returns without damaging compounding.

When you add liquid debt to a momentum portfolio, you’re not trying to boost return, you are trying to protect return.

And two decades of data show that protection is worth more than prediction.

Across 20 years of Indian market history, liquid debt has proved to be:

- A consistent positive-return asset

- A strong hedge during negative periods

- A low-correlation stabilizer

- A drawdown suppressor

- A capital-preservation anchor

- A compounder through chaos

In bull markets, equities take the spotlight.

In crash years, gold takes the spotlight.

But across all years – liquid debt quietly holds the portfolio together.

For any investor running a momentum, tactical, or multi-asset portfolio, liquid debt isn’t a filler allocation.

It is the protection layer that enables everything else to work.