In February 2026, Foreign Institutional Investors (FIIs) turned net buyers in Indian equities – recording their largest monthly inflows in 17 months, with roughly $2.44 billion flowing into Indian stocks.

For many market participants, this felt like déjà vu.

For years, one belief dominated Indian markets:

If FIIs buy, markets rise.

If FIIs sell, markets fall.

And for a long time, that belief was correct. But the February inflows, while positive – also reveal something deeper:

Even when FIIs return, they no longer control the market the way they once did. India’s equity structure has fundamentally changed.

Let’s understand how 👇🏼

For most of the last two decades, Indian equity markets lived under a simple notion:

If FIIs sell, markets fall.

It was true for a long time. India didn’t have enough domestic capital to balance foreign money. A single wave of offshore selling could pull indices down for weeks. And between 2004-2014, FIIs practically were the market.

But the last ten years have quietly changed the structure of Indian equities.

Domestic institutions have grown. Retail investors have exploded. SIP flows have become a monthly engine. And today, even during heavy FII outflows, the market behaves very differently from the past.

Let’s break down what changed – and why India is no longer as vulnerable to foreign flows as it once was.

A decade ago: When FIIs dominated the markets.

To understand how far things have come, it’s helpful to look back.

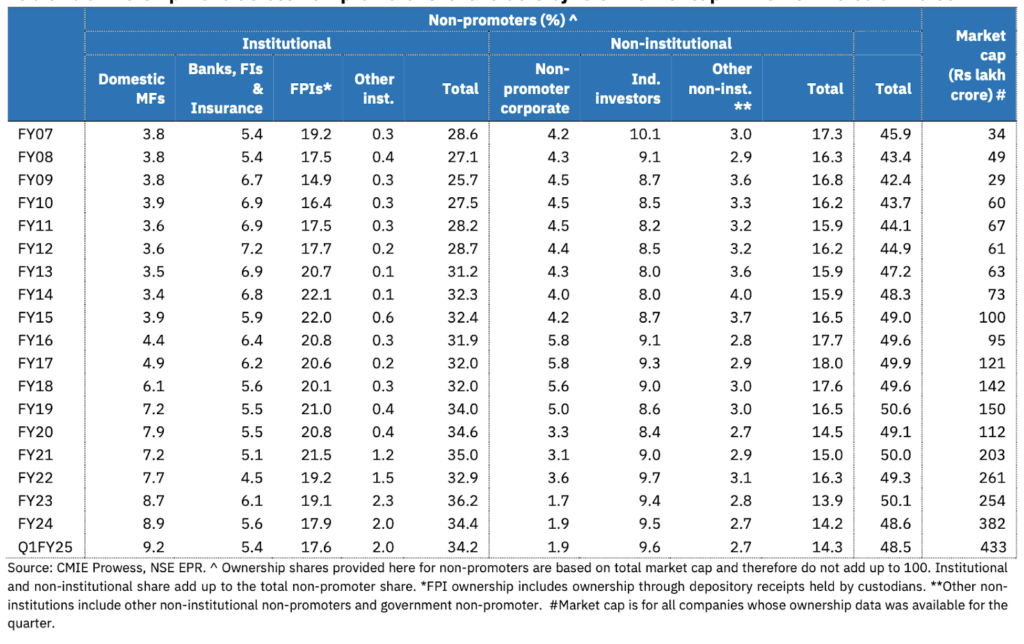

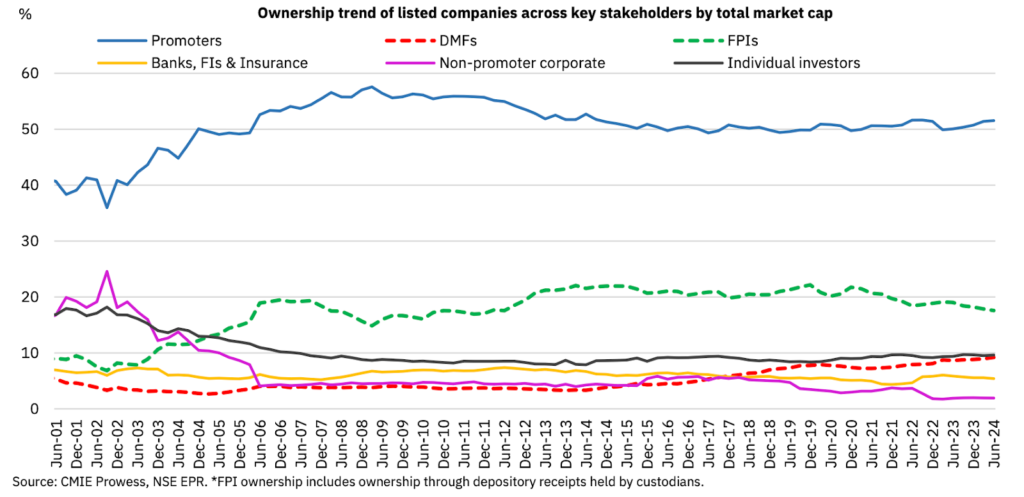

In FY14, FPIs held 22.1% of India’s listed market cap, while domestic mutual funds had barely 3.4%. FPI share in the free float was close to 45-46%, the highest level India had ever seen.

They were the swing force – the ones who dictated liquidity, direction, and sentiment. When they sold, India slipped.

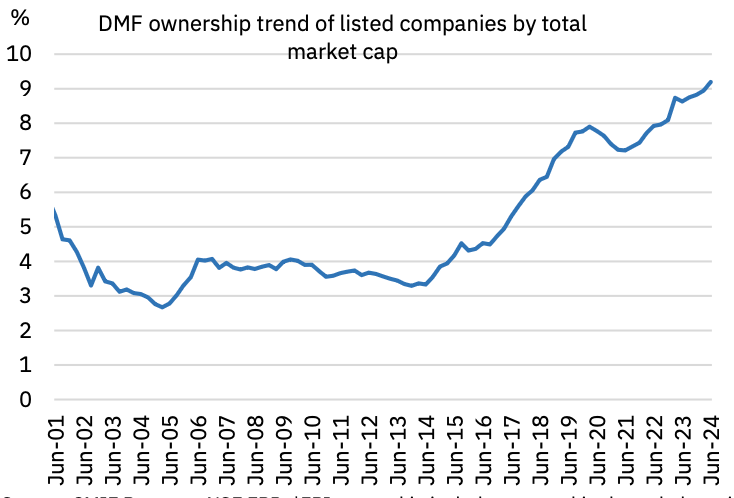

The chart below from the NSE Ownership Tracker captures this era clearly – a period where foreign ownership rose steadily into the mid-2010s.

Back then, domestic capital simply wasn’t big enough to offset large foreign moves.

Fast forward to 2024: A completely different market structure

Over the last few years, India has quietly transitioned from a foreign-dominated market to a three-engine market:

- Foreign investors (FPIs)

- Domestic institutions (mutual funds, insurance, pensions)

- Retail investors

Each plays a meaningful role – but none alone decides the direction.

Here’s the shift in hard numbers.

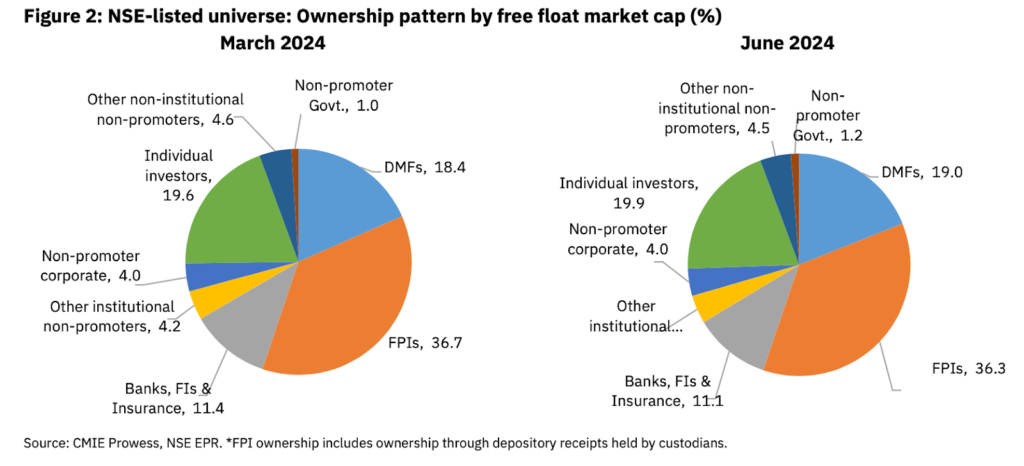

- FPI Ownership has fallen to a 12-year Low. As of June 2024, FPIs hold 17.6% of the total market cap.

Their free-float share is down to 36.3% – almost 10 percentage points below the 2014 peak. Despite this, the value of their holdings still rose to ₹76 lakh crore, simply because the market itself expanded.

This is the first big shift:

Foreign investors remain important, but they no longer dominate India’s free float.

Domestic Mutual Funds have become the market’s centre of gravity

If there’s one number that explains India’s resilience, it’s this: DMF ownership has climbed from 3.4% in FY14 to 8.9% in FY24.

And it didn’t stop there. June 2024: DMFs reached 9.2% of total market cap. In the free float, they own 19% – an all-time high

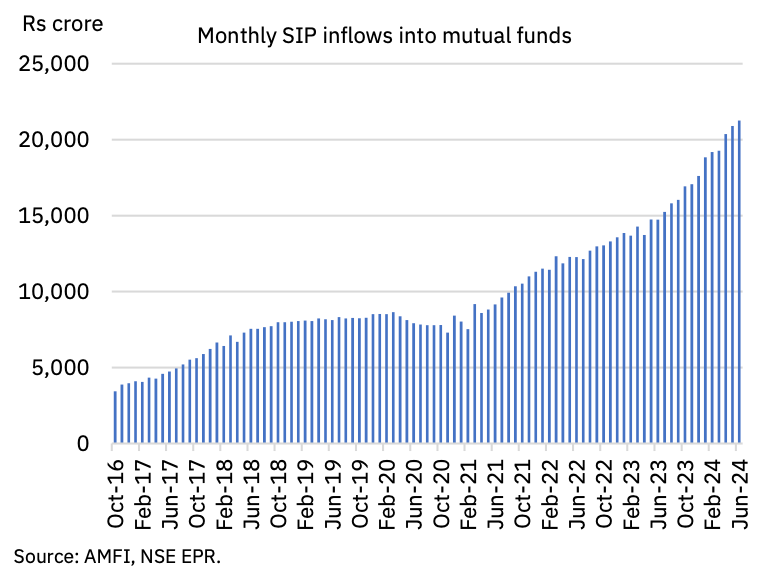

Behind this rise is a cultural shift: the SIP revolution.

Monthly SIP inflows now average ₹20,846 crore, a 9% QoQ jump.

Cumulatively, DMFs have poured ₹8.1 lakh crore into equities since April 2022.

Source: CMIE Prowess, NSE EPR

SIPs behave differently from FII flows. They’re slow, steady, predictable and indifferent to global panic. And that changes everything.

Retail Investors are now a structural force

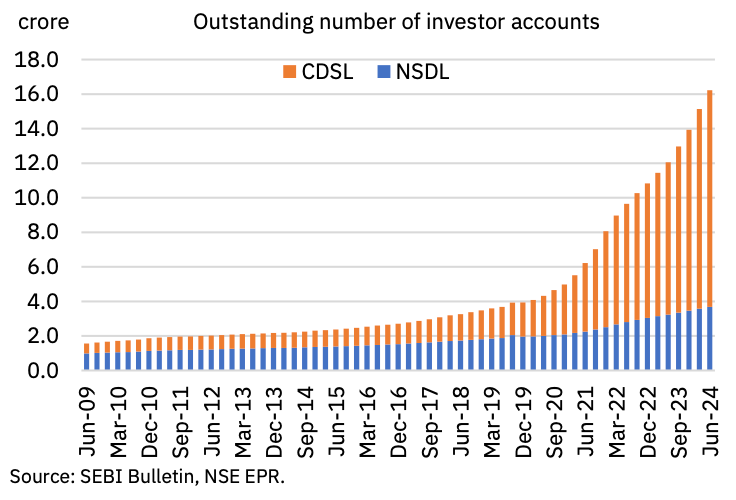

India has added more than 10.7 crore new investor accounts since 2021.

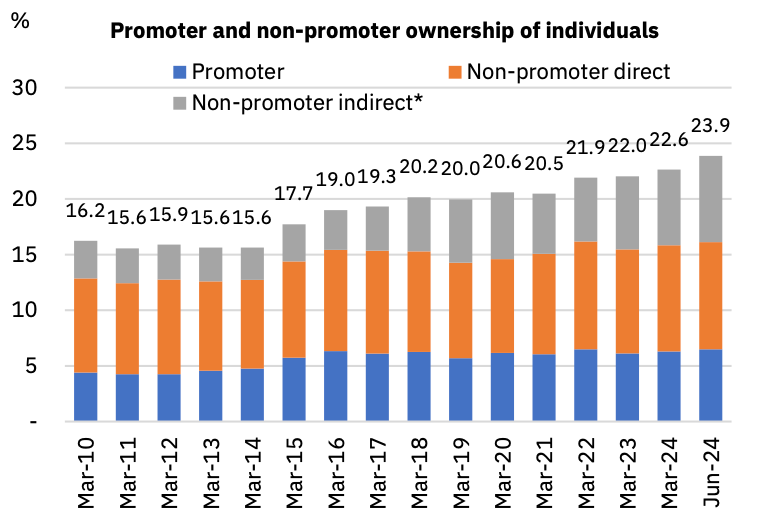

Direct retail ownership is now 9.6%, and when you combine:

- direct stocks

- mutual fund units

- promoter holdings

…Indians collectively own ~24% of the market.

This is up from 15.6% a decade ago.

*Through Mutual Funds

This deeper domestic base softens shocks that once shook the market violently.

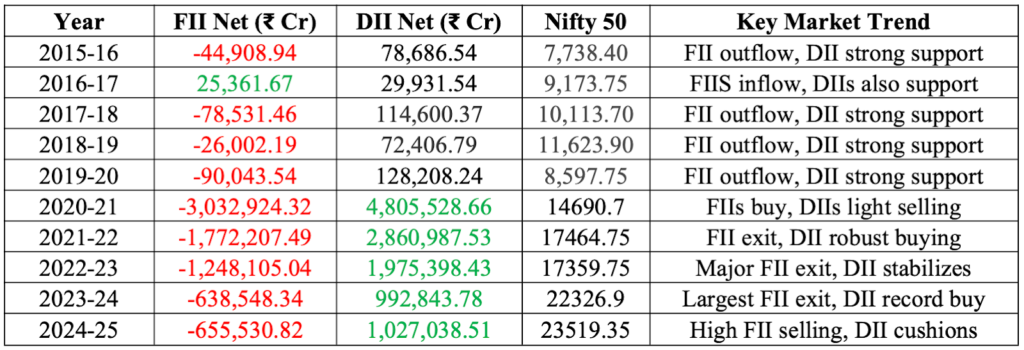

The Flow Story: FIIs sell, DIIs absorb – and markets keep climbing.

Here’s where the shift becomes impossible to ignore.

An independent research paper titled “Indian Equity Flows: FII withdrawals, vs DII market support”.

The pattern is consistent:

FIIs were net sellers in 8 of the last 10 years

DIIs were net buyers in all 10 years

Despite heavy foreign selling, the NIFTY500 Index kept moving higher.

A few examples tell the story:

This isn’t a coincidence. It’s structural.

The research also ran a 10-year regression on the relationship between FII flows and the Nifty:

Correlation: weak (0.41)

R²: 0.165

Result: Statistically insignificant, which means – FII flows do not explain Nifty performance in the long run.

In contrast, DII flows show a strong supportive relationship, especially in high-stress periods.

Foreign money may move the needle for a day.

Domestic money anchors the trend.

What this shift means for investors?

The implications are big and long term. FIIs still matter, but they don’t decide the trend of the markets.

- Large-cap sectors like Financials may still react to FII behavior. But the market’s direction is no longer set offshore.

- Domestic flows are the market’s new backbone. SIP flows don’t care about:

- US inflation

- Fed meetings

- EM risk-off phases

- Global rotation trades

They simply come in every month. This consistency creates a “floor” under the market that never existed before.

Broader Ownership = Greater Resilience

With:

- DMFs at record-high ownership

- Retail participation expanding,

- FPIs less dominant than ever

Market corrections have become shallower and recoveries faster. India is now a market led by domestic conviction, and not foreign mood.

The Bottom Line?

The story the data tells is simple:

In 2014, FIIs were the market.

Now, they are just one part of it.

A decade of rising SIP culture, expanding retail participation, and stronger domestic institutions has rewritten how Indian equities behave.

FII selling still creates volatility – but it no longer derails the market the way it once did. And that shift is one of the biggest reasons behind India’s consistency, resilience, and long-term compounding over the last decade.

The market hasn’t become immune to global flows, it has simply outgrown them.